As a business leader, you are constantly looking for ways to improve your business. If you are in the manufacturing or distribution business, the Supply Chain is where a majority of your costs are and is also where a majority of your opportunities are… and you know it. You have to balance customer-facing issues and risk, manage cash flow and costs while trying to earn a return on investment. You don’t have unlimited resources nor a full-staff of Supply Chain technicians. Your team is in the trenches getting things done. You probably know you are sub-optimized but how can you determine how it is really impacting your business? There is a direct correlation between performance and best practices, but how do you know where to start?

If you do a Google search on Supply Chain Management or Supply Chain Optimization, you will get many advertisements from various technology companies and logistics companies promising the world or articles that discuss advanced strategies or how computer learning and blockchain may revolutionize Supply Chain Management. Don’t get me wrong, I am a HUGE fan of technology, and we work with companies to help them implement technologies to drive significant improvements in their business, but if you are a small or mid-sized business like the ones we typically work with, this can be overwhelming and hard to translate into “how” can you work on improving your business from where you are today and how to get started.

In this article, we are going to discuss the levers of Supply Chain Management. The goal is to educate business leaders to look at the Supply Chain holistically and that there is a structured way we can help companies drive improvements.

The approach that we use with companies uses the following attributes:

- Reliability

- Responsiveness

- Agility

- Cost

- Asset Management Efficiency

Once you understand what you are trying to optimize, you can move on to prioritizing and measuring.

Reliability

Reliability is the ability to consistently deliver what the customer orders when the customer expects it in perfect condition (Perfect Orders). Reliability allows you to look at your business through the lens of your customer.

We worked with a company once that touted a 97% fill rate. However, when we looked at Perfect Orders, that number dropped to just below 30%. Over 70% of the time, they were not meeting customers’ expectations. OUCH!

Responsiveness

Responsiveness is a measure of how fast an order is fulfilled. This starts with the customer order and ends with the customers’ acceptance. Amazon recently announced the investment of $800M to reduce 2-day delivery down to one day. Do your customers expect to get their product fast once they have ordered? How much are you investing?

Agility

Agility is the ability to respond to unplanned external factors and manage risk. Agility measures upside and downside adaptability and value at risk. External factors might be a host of things such as unplanned changes in demand, severe weather, congestion at ports, shortage of raw materials, etc. Agility is about planning for the unplanned and being able to respond when disruptions occur.

An example might be having a hot new product introduced into the market and significantly exceeds forecast. How quickly can your company and underlying suppliers respond? Do you have access to raw materials and enough capacity to build more with current production capacity? Do you have the ability to flex your workforce, work overtime or add a shift? Can your suppliers support the increase? How fast could you respond if you lost your top customer?

Agility shouldn’t only focus on the sales side of the business but also returns. Does your company risk a product recall on the products you manufacture or distribute? How would you support it if it did?

Cost

Cost is exactly what it says, however, we are looking at more than just COGS. We want to look at total Supply Chain costs. This includes COGS + all other Supply Chain costs (direct and indirect).

Optimizing the cost of goods sold (COGS) can potentially reduce costs and have a significant impact on a firm's bottom line. COGS refers to the total expenses incurred in the production of goods or services, and it usually constitutes a substantial portion of a company's overall costs. By focusing on reducing COGS, companies can effectively streamline their supply chain processes and identify opportunities for cost savings.

Since COGS often accounts for a large percentage of a company's costs, even a small reduction in this area can result in significant savings. For instance, let's take the example of a multinational consumer goods company. If they manage to optimize their COGS by finding more cost-effective suppliers, improving manufacturing efficiencies, or leveraging economies of scale, they can directly impact their financial performance. By reducing the costs associated with sourcing raw materials, manufacturing, and distribution, companies can allocate their resources more efficiently and improve their profitability.

Optimizing COGS also allows companies to enhance their competitiveness in the market. By finding ways to produce goods more cost-effectively without compromising quality, companies can offer their products at a more competitive price point. This can attract more customers, increase market share, and ultimately result in higher revenues.

Furthermore, reducing COGS can also help companies respond effectively to changing market conditions. In times of economic downturns or increased competition, having a leaner supply chain and lower production costs can provide a competitive advantage. Companies that can adapt quickly and efficiently by optimizing their COGS are better equipped to navigate challenging times while maintaining profitability.

Asset Management Efficiency

The last area deals with how effectively your company is managing financial resources. In this area, we look at the Cash-to-Cash cycle, Return on Supply Chain Fixed Assets, and Return on Working Capital.

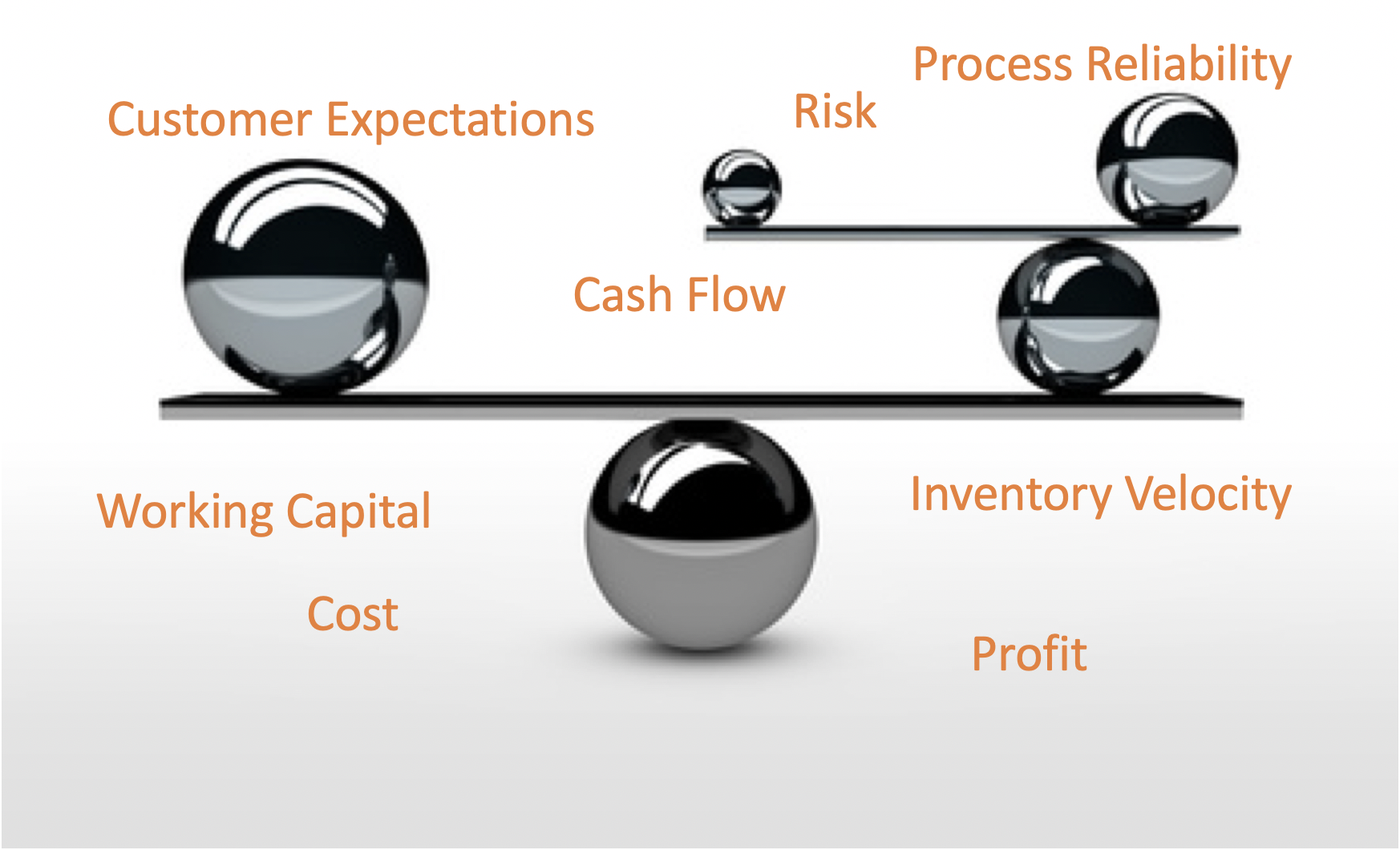

Supply Chain Trade-offs

So now that I have described all the Supply Chain levers, let’s talk about the trade-offs. You see, in many cases, a decision to try to improve one aspect without a properly defined strategy may negatively impact another. For example, several years ago I worked with a company that was having cash flow issues. They had chosen to manufacture in Asia for lower priced goods but didn’t think through how this would affect their working capital needs. They were looking to grow another area of the business and wanted to free up cash from inventory while also being able to respond faster to changing market demands.

Once we evaluated the situation and determined what the company was trying to achieve, we were able to develop a supplier strategy to move the manufacturing to Mexico. The supplier held the inventory as Vendor Managed Inventory here in the US once imported into the US. The company ended up with zero inventory on the balance sheet for this product line, a negative cash-to-cash cycle (generates cash before having to pay suppliers) and an infinite return on working capital. The trade-off though was that the price per unit went up.

Another example you are aware of is Amazon Prime and “free” two-day delivery (and they are continuing to push for faster deliveries). What do you think the trade-offs are for Amazon on fast shipping?

The great thing about understanding the trade-offs is that once your company decides what will be the focus of each Supply Chain, then you can identify projects that will drive improvement in those key metrics.

If you need help with improving your supply chain performance, contact us today to have a conversation about how you can start seeing improvement in your supply chains.

Frequently Asked Questions:

What is the definition of COGS and how does it differ from operating costs?

The definition of COGS (Cost of Goods Sold) contrasts with operating costs within a company's financial accounting framework. COGS encompasses all expenses related directly to the production or acquisition of goods or services that a company sells, while operating costs include a wider range of expenses necessary for ongoing business operations, such as selling, general and administrative (SG&A) costs, and costs related to research and development (R&D). It is important to note that businesses may differ in their classification of costs, with some incorporating COGS expenses into their operating costs. Additionally, certain industries do not uniformly present COGS in their income statements, requiring the derivation of COGS from a combination of various cost components specific to their operations.

How can COGS and gross margin provide insights into a company's operating model, product types, and pricing power when compared to similar companies?

Analyzing a company's cost of goods sold (COGS) and its gross margin can offer valuable insights into various aspects of its operations and performance. By examining these financial metrics, one can gain a deeper understanding of the company's operating model, the types of products it produces, and its pricing power relative to its competitors.

The cost of goods sold represents the direct costs associated with producing the goods or services sold by the company. It includes expenses such as raw materials, labor, and manufacturing overhead. By analyzing the COGS, one can assess how efficiently the company is managing its production costs. A lower COGS compared to competitors may indicate that the company has a more efficient supply chain or manufacturing process, leading to potentially higher profit margins.

Gross margin, on the other hand, is calculated by subtracting the COGS from the total revenue and is expressed as a percentage. It provides insights into the profitability of the company's core business operations. A higher gross margin indicates that the company can command higher prices for its products or has lower production costs relative to its revenue. This can signify pricing power and strong competitive positioning in the market.

When comparing a company's COGS and gross margin to those of similar companies within the industry, one can identify trends and patterns that shed light on the company's competitive advantage or weaknesses. For example, a company with a higher gross margin than its peers may have a differentiated product offering or superior cost management practices. Conversely, a company with a lower gross margin may be facing pricing pressures or inefficiencies in its supply chain.

What does inventory turns represent and how is it calculated? Why is it considered a key metric for managing supply chains?

Inventory turns is a fundamental metric used in the management of supply chains. It essentially indicates how efficiently a company is converting its inventory into sales and cash. The calculation for inventory turns is straightforward: it is determined by dividing the Cost of Goods Sold (COGS) by the average inventory level.

COGS is a figure from the income statement that reflects the costs directly associated with producing goods or services during a defined period, usually a year. On the other hand, inventory represents the value of goods a company currently holds at a specific point in time, which is listed on the balance sheet. To compute inventory turns accurately, the average inventory level over the period considered in the COGS calculation is used.

The reason why inventory turns are considered a critical metric in supply chain management is due to its ability to provide insights into how effectively a company is managing its inventory. A high inventory turnover ratio suggests that a company is selling goods quickly and efficiently, which can translate to reduced carrying costs, lower risk of obsolescence, and improved cash flow. On the flip side, a low inventory turnover ratio indicates that a company may have excess inventory, tying up capital and potentially leading to increased storage costs and reduced profitability. By focusing on optimizing inventory turns, businesses can enhance their operational efficiency, reduce waste, and improve their overall financial performance.

What is gross margin and how is it calculated? Why is it considered a key metric?

Gross margin is a fundamental financial metric that reflects the profitability of a company by indicating the percentage of revenue remaining after deducting the cost of goods sold (COGS). It is calculated by subtracting COGS from revenue and then dividing the result by revenue. The formula for gross margin is as follows:

Gross Margin = (Revenue - COGS) / Revenue

Essentially, gross margin represents the markup that a company adds to its products or services and serves as a measure of its pricing power. This metric is crucial in analyzing a company's financial health and operational efficiency because it reveals how effectively the business is managing its production costs. A high gross margin indicates that the company can cover additional expenses such as sales, marketing, administration, and research and development, while still generating a profit.

Moreover, gross margin provides insights into the competitive positioning of a company within its industry. Industries that heavily rely on research and development to introduce innovative products typically aim for high gross margins to sustain their competitive edge. On the other hand, low gross margins may suggest a business model that is heavily dependent on labor or materials, potentially indicating lower profitability. In summary, gross margin serves as a crucial indicator of a company's financial performance and operational efficiency, making it a key metric in assessing the overall health and competitiveness of a business.

Which industries typically do not have an explicit line item for COGS on their income statement?

Industries that generally do not have a separate line item for Cost of Goods Sold (COGS) on their income statements are those that are not involved in the manufacturing or sale of physical products. This includes service-oriented industries such as consulting, finance, insurance, and other similar sectors where the primary revenue generation is through services rather than through the production or sale of tangible goods.

What is the significance of distribution costs in both COGS and operating costs within supply chain management?

Distribution costs play a significant role in both the Cost of Goods Sold (COGS) and operating costs within supply chain management. These costs are crucial components that encompass various expenses related to the movement of goods through the supply chain. In the context of COGS, distribution costs are an essential factor that contributes to the overall production cost of a product. They represent the expenses incurred in transporting finished goods from production facilities to intermediate locations and ultimately to customers. Additionally, in the case of returns, distribution costs become even more critical as they represent a double impact on the company - not only do returns lead to a decrease in revenue, but they also incur additional costs associated with transporting, storing, restocking, or disposing of the returned items.

On the other hand, when it comes to operating costs, distribution costs are categorized as part of the broader expenses associated with running the day-to-day operations of a company. These costs typically include sales and marketing, finance, customer support, human resources, executive management, and other administrative expenses. Distribution costs are also commonly included in operating costs because some companies choose to account for the expenses related to operating distribution centers within this category. By allocating distribution costs to operating expenses, companies can have a clearer understanding of the total operational expenses incurred in managing their supply chain and logistics activities.

Therefore, the significance of distribution costs in both COGS and operating costs lies in their integral role within supply chain management. By including distribution costs in COGS, companies can accurately calculate the total cost of producing goods and understand the impact of distribution activities on the cost structure. Simultaneously, incorporating these costs into operating expenses provides a comprehensive view of the overall operational expenditures involved in managing the logistics and distribution aspects of the business. This dual representation of distribution costs in COGS and operating costs helps organizations make informed decisions about optimizing supply chain processes, controlling expenses, and enhancing overall efficiency in their operations.

What are the primary elements of COGS and how are they related to supply chains?

The primary elements of Cost of Goods Sold (COGS) are directly intertwined with supply chains. These elements represent the costs incurred in the process of procuring raw materials, transforming them through manufacturing or other processes, managing the finished products in inventory, and transporting them to various locations, including to the end customers. Additionally, the process includes handling returns, which can have a significant impact on revenue due to additional costs incurred for transportation, storage, restocking, or disposing of the items. These different stages of the supply chain are all integral parts of the COGS calculation.

Within these elements of COGS, inventory carrying costs play a crucial role. These costs encompass various expenses such as storage, obsolescence, shrinkage, insurance, handling, management, and financial expenses. Financial costs specifically relate to the cost of money tied up in inventory over time. This includes the cost of financing the inventory if it is financed and the opportunity cost of using that capital elsewhere. It is typically calculated as a company's weighted average cost of capital (WACC) multiplied by the inventory value held over a specific period.

Moreover, it is important to note that financial costs and inventory financing costs are subject to fluctuations based on interest rates. For example, a low-interest rate environment can lead to lower inventory carrying costs, while increasing interest rates can raise these costs. Understanding and managing these primary elements of COGS in relation to supply chains is essential for businesses to optimize their operations and profitability.

What are the supply chain-related costs found in the operating costs section of a company's income statement?

Supply chain-related costs found in the operating costs section of a company's income statement are expenses that are directly tied to the production and distribution activities of the company. These costs include but are not limited to procurement costs, manufacturing costs, transportation costs, warehousing costs, and logistics costs. In essence, they encompass all the expenses incurred in the process of sourcing raw materials, manufacturing products, managing inventory, and delivering the final goods to customers. Properly accounting for these supply chain-related costs is essential for a comprehensive analysis of a company's financial performance and for facilitating meaningful comparisons between companies within the same industry.

How do revenue, COGS, and operating costs relate to supply chain and related costs?

Supply chain and related costs play a crucial role in various areas of a company's income statement, including revenue, cost of goods sold (COGS), and operating costs.

In terms of revenue, supply chain management impacts key elements such as trade promotions, markdowns, and returns. Trade promotions involve collaborations between manufacturers and retailers to offer periodic price reductions, influencing consumer behavior and driving sales. Markdowns, typically associated with clearing excess inventory, can result from poor demand forecasts or product obsolescence. Returns also impact revenue by reducing sales and incurring additional costs for transportation, storage, and restocking.

Moving on to COGS, various components are intertwined with the supply chain. Material procurement, manufacturing processes, inventory management, and transportation all contribute to the final cost of goods sold. Returns pose a particular challenge as they not only decrease revenue but also incur costs for handling, storing, and possibly disposing of returned items.

In the operating costs section of an income statement, supply chain-related expenses include distribution costs, which may be part of both COGS and operating costs for some companies. Inventory carrying costs encompass various expenses such as storage, obsolescence, insurance, and financial costs, which reflect the cost of holding inventory over time. Fluctuations in interest rates can impact these financial costs and influence overall inventory carrying costs.

Additionally, customer service plays a crucial role in operating costs, particularly in supply chain management. Customer inquiries about delivery dates or returns often require efficient coordination within the supply chain. Marketing and advertising expenses, while part of the marketing function, contribute significantly to demand management, an essential aspect of effective supply chain management.

Therefore, supply chain and related costs are intricately connected to revenue generation, cost of goods sold, and operating expenses in a company, emphasizing the importance of efficient supply chain management for overall financial performance.

How are Cost of Goods Sold (COGS) related to supply chain management and how should it be approached?

Cost of Goods Sold (COGS) plays a vital role in supply chain management as it serves as a key financial term within this domain. In the context of SCM, COGS represents the total cost of producing or acquiring products that have been sold during a specific period. Essentially, it encompasses various expenses associated with the production or procurement of goods, such as raw materials, labor, and overhead costs. Given that COGS is a reflection of the costs directly tied to the supply chain, it is crucial in understanding and optimizing the financial performance of a company's operations.

Approaching COGS in supply chain management involves a comprehensive analysis of cost components and their impact on overall operational efficiency. By accurately calculating COGS, businesses can gain insights into their production expenses, identify cost-saving opportunities, and enhance decision-making processes. Furthermore, a detailed understanding of COGS enables organizations to evaluate profitability, assess pricing strategies, and optimize inventory management practices. In essence, a strategic approach to managing COGS within the supply chain is essential for optimizing operational performance, enhancing financial visibility, and achieving sustainable growth.

How do inventory carrying costs impact supply chain management and COGS?

Inventory carrying costs have a direct impact on supply chain management and the cost of goods sold (COGS). These costs, such as storage, obsolescence, shrinkage, insurance, handling, and financial costs, contribute to the overall expenses associated with storing and managing inventory. Financial costs, including the cost of financing the inventory and the opportunity cost of tied-up capital, play a significant role in inventory carrying costs. These costs are typically calculated based on a company's weighted average cost of capital (WACC) multiplied by the value of inventory held.

The impact of inventory carrying costs on supply chain management is profound, as they directly affect a company's bottom line and profitability. By adding significant overhead expenses, inventory carrying costs put pressure on supply chain managers to optimize inventory levels and streamline processes to minimize these expenses. Failure to manage these costs efficiently can lead to reduced profitability and competitive disadvantage in the market.

Moreover, these costs also influence the calculation of COGS. Higher inventory carrying costs translate to increased expenses related to production and distribution, which in turn affect the COGS. When COGS are higher due to inflated inventory carrying costs, it can directly impact the company's profitability and financial health. Supply chain managers need to strike a balance between maintaining adequate inventory levels to meet demand and minimizing carrying costs to ensure optimal COGS and overall operational efficiency.

What are the elements related to supply chain management within financial statements?

Within financial statements, there are key elements that are closely intertwined with supply chain management. These elements play a crucial role in managing various aspects of the supply chain to enhance overall efficiency and effectiveness. Examples of these elements include cost optimization, asset optimization, and cash-to-cash optimization.

Cost optimization within financial statements is linked to strategies aimed at reducing the costs associated with goods sold while simultaneously increasing revenues. This element focuses on identifying opportunities to streamline operations, negotiate better deals with suppliers, and improve overall cost-effectiveness throughout the supply chain process.

Asset optimization, another important element related to supply chain management within financial statements, revolves around minimizing the physical assets required for manufacturing and transporting products. By efficiently managing and utilizing assets such as inventory, equipment, and facilities, companies can enhance productivity, reduce waste, and improve profitability.

Furthermore, cash-to-cash optimization is a key element that emphasizes minimizing the amount of cash tied up in various aspects of the supply chain, including inventory, receipts, and payments. This element is essential for maintaining healthy working capital levels, improving cash flow efficiency, and reducing financial risks associated with inventory management and payment cycles.

In summary, the elements related to supply chain management within financial statements, such as cost optimization, asset optimization, and cash-to-cash optimization, provide valuable insights into how businesses can strategically manage their supply chain operations to achieve optimal performance and financial outcomes.

What are the key cost elements associated with revenue in the context of supply chain management?

Key cost elements associated with revenue in the context of supply chain management include trade promotions, markdowns, and returns. Trade promotions involve periodic price reductions agreed upon by manufacturers and retailers to stimulate sales. While they can be strategically planned around seasons or events, trade promotions can also be implemented reactively to address revenue gaps or competitive pressures. Markdowns are another cost element that impact revenue, often indicating the need to clear out excess or unwanted inventory through price reductions. Factors contributing to markdowns include dated inventory, declining product appeal, and inaccurate demand forecasting. Returns also play a role in reducing revenue as they represent product returns from customers due to various reasons such as defects, dissatisfaction, or damaged goods. Managing these cost elements effectively is crucial for optimizing revenue in supply chain operations.

How do trade promotions, markdowns, and returns influence supply chain management and revenue?

Trade promotions, markdowns, and returns each play a crucial role in influencing both supply chain management and revenue within a business. Trade promotions, for instance, are collaborative efforts between manufacturers and retailers that involve periodic price reductions to stimulate sales. While these promotions can boost demand and increase sales volume, they also impact revenue by adjusting final sales prices. This adjustment affects the overall revenue generated from each sale during the promotion period.

Markdowns, on the other hand, are often necessary to clear out unwanted inventory that may be aging, no longer in demand, or due to forecasting errors. While markdowns help in managing excess stock, they directly impact revenue by reducing the selling price of the products. Additionally, markdowns can also increase supply chain costs, as the products may need to be moved quickly or stored for longer periods due to lower demand.

Returns are another aspect that significantly influences both revenue and supply chain management. When customers return products, it not only leads to a direct negative impact on revenue but also incurs additional costs for transportation, storage, restocking, or disposal of the returned items. This affects the profitability of sales transactions and requires careful management within the supply chain to handle returns efficiently.

In conclusion, trade promotions, markdowns, and returns are closely intertwined with supply chain management and revenue. Each of these aspects directly impacts the financial performance of a business and requires careful planning and execution to optimize revenue generation while effectively managing the associated costs within the supply chain.